It is not a coincidence that U.S. economic growth has been more than a full percentage point slower than the post-WWII average for 15 years at a time when new business formation rates have fallen near four-decade lows.

For fifteen years now, the United States has been caught in the grip of a persistent economic growth crisis. Many might find that statement confusing or even ridiculous – aren’t we in the midst of the longest economic expansion in history?

Indeed, we are. Last July, the current economic expansion, which began at the end of the Great Recession in June of 2009, broke the previous record of 120 months of consecutive economic growth, which ran from March of 1991 to March of 2001. The economy has now been growing for 127 consecutive months and looks likely to continue expanding for many months to come.

So, where’s this growth crisis?

As the late great radio commentator Paul Harvey would say: and now for the rest of the story…

For 54 years following World War II – from 1947 and 2000 – the U.S. economy grew at an average annual rate of 3.5 percent. Not every year – some years were slower, some were faster – but, on average, for 54 years, the U.S. economy grew at an average rate of 3.5 percent.

By stark contrast, the economy has not grown at 3 percent or better, on a year-over-year basis, since 2005 – 15 years ago. And since the end of the Great Recession in 2009 – that is, during this record-breaking period of sustained growth – the economy has grown at the lackluster annual pace of just 2.3 percent.

The difference between growth of 2.3 percent and 3.5 percent may not seem significant, but in an economy the size of the U.S. economy percentage points matter – a lot. Had the economy grown at 3.5 percent rather than 2.3 percent since emerging from recession in 2009, economic output last year alone would have been $2.4 trillion – or 12 percent – greater than it was.

By the way, $2.4 trillion is roughly the size of France’s economy – the world’s seventh largest. American businesses, households, and consumers missed out on additional economic activity equivalent to the world’s seventh largest economy, last year alone.

Over a 25-year period, the difference between a U.S. economy growing at 3.5 percent annually rather than 2.3 percent is an additional – that is, on top of the output generated at 2.3 percent – $116 trillion in economic output.

That’s a very big number and hard to wrap one’s head around, so let’s put that into some practical perspective.

On November 1st, the Treasury Department announced that U.S. national debt had surpassed $23 trillion for the first time.

Meanwhile, the American Society of Civil Engineers, which grades the nation’s infrastructure in a report issued every four years, has given America’s infrastructure a D+ and said that it would cost $4.5 trillion to make the improvements necessary to avoid losing trillions in economic output and millions of jobs in coming years.

$23 trillion in national debt plus $4.5 trillion in infrastructure needs equals $27.5 trillion.

Now, since the end of World War II, the U.S. government has consistently collected about 18 percent of GDP in tax receipts. It’s an interesting phenomenon that actually has a name – Hauser’s law – after William Hauser, a financial analyst who first pointed out the pattern in 1993. Regardless of where marginal tax rates happen to be, the government has consistently collected about 18 percent of GDP in federal tax receipts.

Eighteen percent of $116 trillion – the additional output that average annual growth of 3.5 percent would generate on top of 2.3 percent growth – is $21 trillion.

So, with the additional federal tax receipts generated by growth of 3.5 percent, over 25 years the United States could either pay down nearly all of its current national debt, or pay down 72 percent of the current debt and rebuild the nation’s infrastructure from coast to coast – assuming Congress didn’t spend the additional revenue on something else.

That’s the difference between 3.5 percent growth and 2.3 percent growth. And that’s just in terms of federal tax receipts. Think of the implications for job creation, wages, opportunity, and economic security.

Some say it’s unreasonable to expect an economy the size of the U.S. economy to grow at or about 3.5 percent on a sustained basis. Except that it did for 54 years after World War II. And it did as recently as the 1990s – over the entire decade.

Given the evidence, it seems more reasonable to argue that the economy can grow at 3.5 percent than to argue that it can’t.

Unfortunately, the most recent data is not encouraging. On January 30th, the Commerce Department announced that the economy grew at an annualized 2.1 percent in the fourth quarter of 2019, and by just 2.3 percent for the year overall – the slowest pace in three years. Two days before, the nonpartisan Congressional Budget Office announced that it expects growth to slow to just 1.7 percent after 2021 and remain below 2 percent for the remainder of the decade.

Exacerbating the effects of slow growth is the distribution of that sluggish growth, which has been highly concentrated. In the five years following the end of the Great Recession, more than half of all new business formation occurred in just 20 counties clustered around five cities. More than half of the jobs in the nation’s most innovative industries are located in just 41 counties, according to a recent report from the Brookings Institution, and just 31 counties of the more than 3,000 nationwide account for a third of the nation’s economic activity.

The inability to accelerate economic growth is all the more astonishing in light of policy attempts over the last ten years that can only be described as Herculean:

- The $830 billion American Recovery and Reinvestment Act of 2009;

- Massively accommodative monetary policy by the Federal Reserve, including five straight years of zero percent interest rates and three rounds of quantitative easing. On October 30th, the Fed cut interest rates for third time since July;

- Historic deficit spending, adding trillions to the national debt;

- The Tax Cuts and Jobs Act of 2017, the most significant tax reform since 1986; and,

- The Trump Administration’s much-touted deregulation efforts.

Despite these extraordinary efforts, economic growth remains stuck at about 2.3 percent. It’s as if policymakers are digging in the wrong place.

This long period of sub-par growth has led to a number of serious socio-economic problems, including persistent job anxiety despite a historically low unemployment rate; simmering dissatisfaction with the distribution of economic gains; decades of wage stagnation, although some progress has been made more recently; wide and worsening income and wealth inequality; pockets of rising poverty despite a reduction in overall poverty since 2014; and, the number of Americans reliant on government programs like food stamps and disability insurance near all-time highs.

Two grotesquely vivid symptoms of persistent economic anxiety and hopelessness are suicides, which have increased for thirteen straight years and now claim more American lives than traffic accidents or homicides, and an opioid crisis that killed 70,000 Americans last year alone. To put that in perspective, the nation lost 56,000 lives in 15 years of the Vietnam War. In a report issued in September, Congress’ Joint Economic Committee stated that the current rate of so-called “deaths of despair” – by suicide, drug overdose, or alcohol abuse – “far surpasses anything seen in America since the dawn of the 20th century.”

Such problems – and the anger, cynicism, and populism they inspire – have, over time, undermined public confidence in corporations and government, led to charges that America’s political and economic system is not only unfair but “rigged,” and threatened the social cohesion and consensus that a thriving democracy requires.

A poll released in October of last year showed that more than a third – 36 percent – of millennials say that they approve of communism, and a full 70 percent say that, given the choice, they would “likely” vote for socialist candidate for president. To put that threat in perspective, data analyzed by the Pew Research Center has shown that the millennial generation surpassed the Baby Boomer generation in 2019 to become the largest segment of the adult population – 73 million voters.

It’s hard not to conclude that the consensus for American capitalism is in serious jeopardy.

Against this rather stark backdrop, building a more robust, accessible, inclusive economy – one that “works for everyone” and that delivers more equitably shared prosperity – has emerged as America’s most urgent domestic challenge.

And meeting that challenge starts with accelerating economic growth back to the 3.5 percent annual growth on a sustained basis that the nation enjoyed for more than five decades after World War II, and as recently as the 1990s. Sustained growth at or above the historical rate would produce the jobs necessary to end under-employment and job anxiety, the opportunity necessary to accelerate socio-economic mobility, the rising real wages needed to narrow the income gap and reduce poverty, and the additional tax revenue necessary to reduce budget deficits and begin paying down the nation’s long-term debt.

Which raises the fundamental “zeitgeist” question confronting America in 2020 – where does economic growth really come from?

Where Does Economic Growth Come From?

Over most of economic history, it had been widely assumed that economic growth comes from growth in one or both of the two principal components of an economy – labor and capital (machinery). For an economy to grow, it was thought, either the supply of labor had to expand or capital intensity had to somehow increase. Indeed, growth in the U.S. labor force driven by the baby boom generation and women entering the workforce in large numbers beginning in the 1960s helps explain robust post-war economic growth.

But in 1957, American economist Robert Solow demonstrated that, while growth in the supply of labor and capital matter, most of economic growth comes from gains in productivity – more output per unit of input – driven by innovation. As businesses and workers become more efficient and productive, costs fall, profits and incomes rise, demand expands, and economic growth and job creation accelerate.

Solow’s identification of innovation-driven productivity gains as the driver of economic growth has been echoed by economists ever since. Fellow Nobel laureate Paul Krugman has observed:

“Productivity isn’t everything, but in the long run it’s almost everything. A country’s ability to improve its standard of living over time depends almost entirely on its ability to raise its output per worker…Compared with the problem of slow productivity growth, all our other long-term economic concerns – foreign competition, the industrial base, lagging technology, deteriorating infrastructure, and so on – are minor issues.”

Solow’s growth model is one of the great economic insights of all time, and for his work Solow was awarded the Nobel Prize in 1987, the National Medal of Science by President Clinton in 1999, and the Presidential Medal of Freedom by President Obama in 2014.

The great significance of Solow’s work is that it not only defined the nature of economic growth, it also identified its principal source. That’s because economists have long understood that innovation – particularly major, transformative, or “disruptive” innovation – comes disproportionately from new businesses, or “startups.”

And that makes sense – entrepreneurs typically launch a new business because they have something new: a new product or new service, or some innovative twist on an old idea. Existing firms do innovate, but mostly at the margin. They don’t innovate in the same way or to the same extent as new businesses because they’re heavily invested in the establishment – their product, their service, their way of doing things. And they’re definitely not interested in disruption.

It’s almost always an outsider who shakes things up. In fact, virtually all the transformative innovations that have defined the economic landscape over the past 150 years – the steam engine, the cotton gin, railroads, the telephone and telegraph, electrification, the automobile, the airplane, the computer, air conditioning and refrigeration, countless applications of the Internet, all the way up to and including wireless communication – came from entrepreneurs.

Joseph Schumpeter called the constant process of insurgents overtaking and replacing incumbents “creative destruction” and proclaimed it to be the driving force of capitalist progress.

In addition to innovation, research conducted since 2009 has shown that startups also account for virtually all net new job creation.

From the standpoint of innovation, economic growth, and job creation, thriving entrepreneurship is the beating heart – the very soul – of a healthy, productive, and growing economy.

The Engine of Innovation and Economic Growth is Breaking Down

Unfortunately, as scholars at the Kauffman Foundation, the Brookings Institution, and elsewhere have documented, entrepreneurship in America is in trouble. Not everywhere, of course; in places like Silicon Valley, Austin, TX, Boulder, CO, and Cambridge, MA entrepreneurship is thriving. But in broad terms, entrepreneurship in America is struggling.

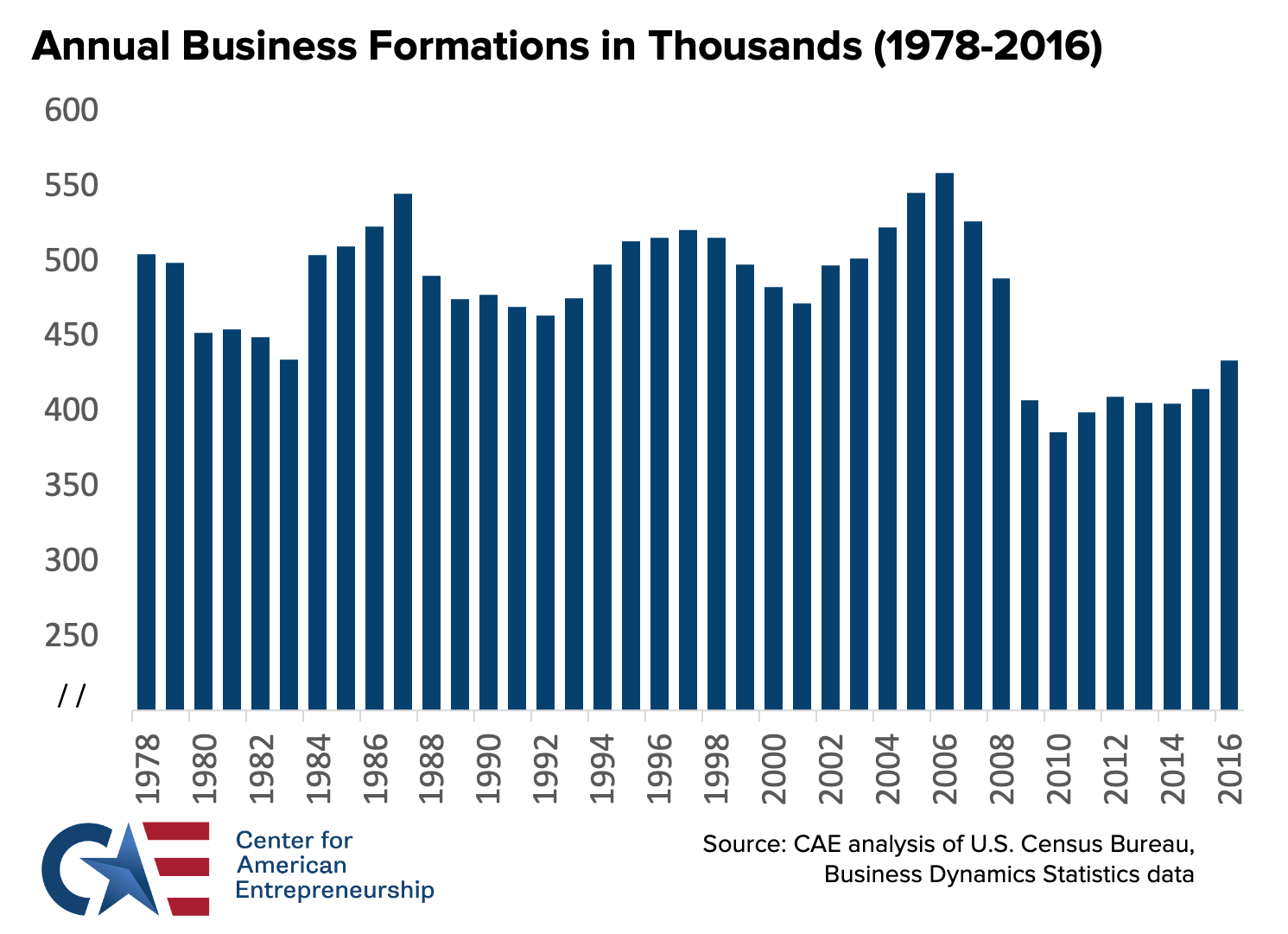

After remaining remarkably consistent for decades, the number of new businesses launched in the United States peaked in 2006 and then began a precipitous decline – a decline accelerated by the Great Recession.

From 2002 to 2006, the economy produced an average of 524,000 new employer firms each year. Since 2009, however, the number of new business launched annually has dropped to about 400,000, meaning the United States currently faces a startup deficit of 100,000 new firms every year – and a million missing startups since 2009.

Even more alarming, economists Robert Litan and Ian Hathaway have shown that rates of entrepreneurship – the fraction of all U.S. businesses that are new – have fallen near a four-decade low, and that this decline is occurring in all 50 states, in all but a handful of the 360 metro areas they examined, and across a broad range of industry sectors.

The U.S. economy is becoming less entrepreneurial, more concentrated among large incumbent companies, less “dynamic.”

And, as Robert Solow’s growth model would predict, productivity growth in recent years has been only half the historical average. On November 6th, the Labor Department announced that U.S. productivity actually declined in the third quarter.

Nobel laureate economist Edward Prescott and his colleague Lee Ohanian from Stanford University have argued that the economy’s anemic performance in recent years is principally due to the plunge in productivity growth – caused by the dramatic decline in startups.

“The most recent period of rapid productivity growth in the U.S. — and rapid economic growth — was in the 1980s and ‘90s and reflected the remarkable success of new businesses in information and communications technologies, including Microsoft, Apple, Amazon, Intel, and Google. These new companies not only created millions of jobs but transformed society, changing how much of the world produces, distributes, and markets goods and services.

Sadly, the annual rate of new business creation is about 28 percent lower today than it was in the 1980s, according to our analysis of the U.S. Census Bureau’s Business Dynamics Statistics. Getting the U.S. economy back on track will require a much higher annual rate of new business startups.”

Here’s the bottom line: economic growth comes principally from gains in productivity, driven by innovation, which comes disproportionately from startups – rates of which have fallen at or near four-decade lows.

Given the importance of thriving entrepreneurship to innovation, economic growth, job creation, and expanding opportunity, such circumstances amount to nothing short of a national emergency.

A Washington Awakening

Fortunately, Washington is finally waking up to this reality.

On March 6, 2019, the first-ever bipartisan Entrepreneurship Caucus was launched in the United States Senate. The Caucus is co-chaired by Senator Amy Klobuchar (D-MN) and Senator Tim Scott (R-SC), and also includes Senators Roy Blunt (R-MO), Bob Casey (D-PA), Chris Coons (D-DE), Joni Ernst (R-IA), Lindsey Graham (R-SC), Maggie Hassan (D-NH), John Hoeven (R-ND), James Inhofe (R-OK), Doug Jones (D-AL), Jerry Moran (R-KS), Gary Peters (D-MI), David Perdue (R-GA), and Kyrsten Sinema (D-AZ), and Tina Smith (D-MN).

Then, on October 2, 2019, a new bipartisan Entrepreneurship Caucus was launched in the House of Representatives, co-chaired by Rep. French Hill (R-AK), Rep. David Schweikert (R-AZ), Rep. Steve Chabot (R-OH), Rep. Bill Foster (D-IL), Rep. Stephanie Murphy (D-FL), and Rep. Marc Veasey (D-TX).

The establishment of a bipartisan Entrepreneurship Caucus in both chambers of Congress for the first time is an enormously significant development for American entrepreneurship because caucuses are an important part the policymaking machinery in Washington. Caucuses and other “Congressional Member Organizations” help bring structure, coherence, and consensus to multi-faceted topics like entrepreneurship. They enable Members of Congress to exchange information and ideas on topics of common interest, participate in events and inquiries, and generally facilitate interactions among Members who might not otherwise have the opportunity to work together.

There are hundreds of caucuses in both the House and Senate. But, astonishingly, there had never been an active caucus dedicated to entrepreneurship in either the House or Senate – until last year. Establishment of entrepreneurship caucuses was a top priority for CAE when I and my colleagues launched the organization in July of 2017.

And both new caucuses have already demonstrated their value and potential. On September 24, 2019, CAE helped arrange a Women’s Entrepreneurship Roundtable with the Senate Entrepreneurship Caucus. Twenty-two women entrepreneurs from across the United States traveled to Washington, DC at CAE’s invitation for the two-hour discussion, which focused on the unique issues, challenges, and obstacles that confront women entrepreneurs, and what policymakers can do to help. Caucus co-chairs Senator Amy Klobuchar (D-MN) and Senator Tim Scott (R-SC) served as hosts, and Wendy Guillies, president and CEO of the Kauffman Foundation, served as moderator.

The roundtable showcased the remarkable talent and innovative capacity of America’s women entrepreneurs – and also their unique needs and vulnerabilities. In particular, the discussion revealed the critical importance to women entrepreneurs of four “mobility” issues: healthcare, childcare, student debt, and retirement security.

On that same day, September 24, 2019, Senate Entrepreneurship Caucus co-chairs Senator Amy Klobuchar and Senator Tim Scott introduced the Enhancing Entrepreneurship for the 21st Century Act. The legislation directs the Secretary of Commerce to conduct a two-year analysis of the multi-decade decline in new business formation rates, including likely contributing factors and economic implications. The analysis will be the most comprehensive ever conducted of the state of American entrepreneurship, bringing to bear all the data and analytic capacities of U.S. government agencies.

On November 1, 2019 – just four weeks after the establishment of the Caucus – the six co-chairs of the new House Entrepreneurship Caucus introduced the Act in the House of Representatives. In a statement, Caucus co-chair Rep. French Hill said:

“One thing that we know for certain is that small business entrepreneurs and startups are responsible for the majority of new innovation, job creation, and economic growth. However, as the rate of new business formation continues to decrease, Congress needs comprehensive answers on how to enact pro-growth policies for a 21st century economy…Working with entrepreneurs, business leaders, and economists to identify the root causes of the startup slump is a critical step to unleashing a new generation of small business growth.”

Other entrepreneurship-focused legislation introduced in recent months includes:

- The Research and Development Tax Credit Expansion Act: Introduced on July 23rd by Senators Maggie Hassan (D-NH) and Thom Tillis (R-NC), the bill will expand startups’ ability to apply the R&D tax credit to their payroll taxes rather than income taxes, which many startups don’t have.

- The Workforce Mobility Act: Introduced by Senators Todd Young (R-IN) and Chris Murphy (D-CT) on October 16th, the bill would ban the enforcement of noncompete agreements in all but the most necessary of circumstances. The legislation was introduced in the House on January 29, 2020 by Rep. Scott Peters (D-CA), Rep. Mike Gallagher (R-WI), and Rep. Anna G. Eshoo (D-CA).

- The PROGRESS Act: Introduced by Senator Ron Wyden (D-OR) on October 30th, the bill will improve startups’ access to capital by providing a first employee tax credit up to 25 percent of the first employee’s wages, and by providing angel investors with a tax credit for investing in new businesses;

In addition to these recently introduced bills, the SECURE Act, introduced in the House by Ways and Means Chairman Richard Neal (D-MA) and Ranking Member Kevin Brady (R-TX), and in the Senate by Finance Committee Chairman Chuck Grassley (R-IA) and Ranking Member Ron Wyden (D-OR), was signed into law by President Trump on December 20, 2019 as part of federal government’s year-end spending bill. The legislation modernizes retirements security law to enable small businesses and startups to band together to provide multiple-employer 401(k)-like retirement savings products to their employees.

Other critical aspects of a pro-entrepreneurship agenda include increasing research and development investment; accelerating the commercialization of federally-funded innovation; education reform and training to ensure 21st century workforce readiness; immigration reform to attract and retain the world’s best talent; improving access to capital; reducing regulatory complexity and uncertainty; addressing healthcare, childcare, and record student debt as obstacles to entrepreneurship, particularly among women and people of color; and addressing provisions of the tax code that disadvantage new businesses.

A revitalization of American entrepreneurship is the essential pathway back to the robust economic growth and opportunity the American people need and deserve.

With an Entrepreneurship Caucus now established in both the House and the Senate, America has an unprecedented opportunity to finally “dig in the right place” and build a stronger, more accessible, and inclusive economy – one that truly works for everyone.