The Relative Resilience of Venture Capital Deals During COVID-19 So Far

September 2, 2020

September 2, 2020

Ian Hathaway

Ian Hathaway

As the COVID-19 pandemic began to take shape in the U.S. in mid-March, two concerns emerged around venture-backed entrepreneurship. First, would investors pull back on financings, in particular financings into new companies, making it difficult for startups to secure the funding needed to navigate an economic downturn? Second, would startups located outside the leading cities have an especially difficult time securing financing? With an economy in freefall and all sectors vulnerable to large shocks, many thought it was probable that venture capital, and the startups financed by it, would be hit hard too—perhaps even more so than other areas.

These concerns were sensible. Venture capital is driven by networks and interpersonal relations. Both place a premium on physical proximity—something that social distancing and shelter-in-place guidelines undermine. Venture capitalists are highly concentrated geographically, particularly in the San Francisco Bay Area. Distancing could make it difficult for entrepreneurs to raise fresh capital from investors where a preexisting relationship hasn’t been established, particularly for the many entrepreneurs around the country without strong ties inside the Bay Area network.

My analysis of the data suggests that many of these concerns have been overblown, at least so far. In a rush to make real-time predictions as the crisis unfolded, many pundits and observers failed to appreciate the ability of venture capitalists to adapt. Likewise, some analysts overestimated the drop in venture activity early on by not accounting for the systematic reporting lags in venture capital databases. These simple adjustments show, in near-real-time, that the drop in venture deal activity has been relatively modest so far—certainly nowhere near the collapse that was envisioned by some early on, or, in comparison to the declines seen in the labor market and broader economy.

Data that have been adjusted to account for these systematic reporting lags suggest a relatively small drop in venture deal activity in 2020 so far. Lag-adjusted venture deal activity through the first half of 2020 fell 3% compared with the previous six months (second half of 2019) and 6% versus the year before (first half of 2019). Lag-adjusted data do suggest, preliminarily, a single-quarter drop in deal activity between Q1-2020 and Q2-2020 that is larger. However, a more credible comparison of higher-frequency changes within 2020 can’t occur until after the next quarterly release when the Q2 data are first revised (due out in mid-October). The analysis here will make comparisons through the lens of the pandemic as a single, half-year event (two-quarters of data; January through June).

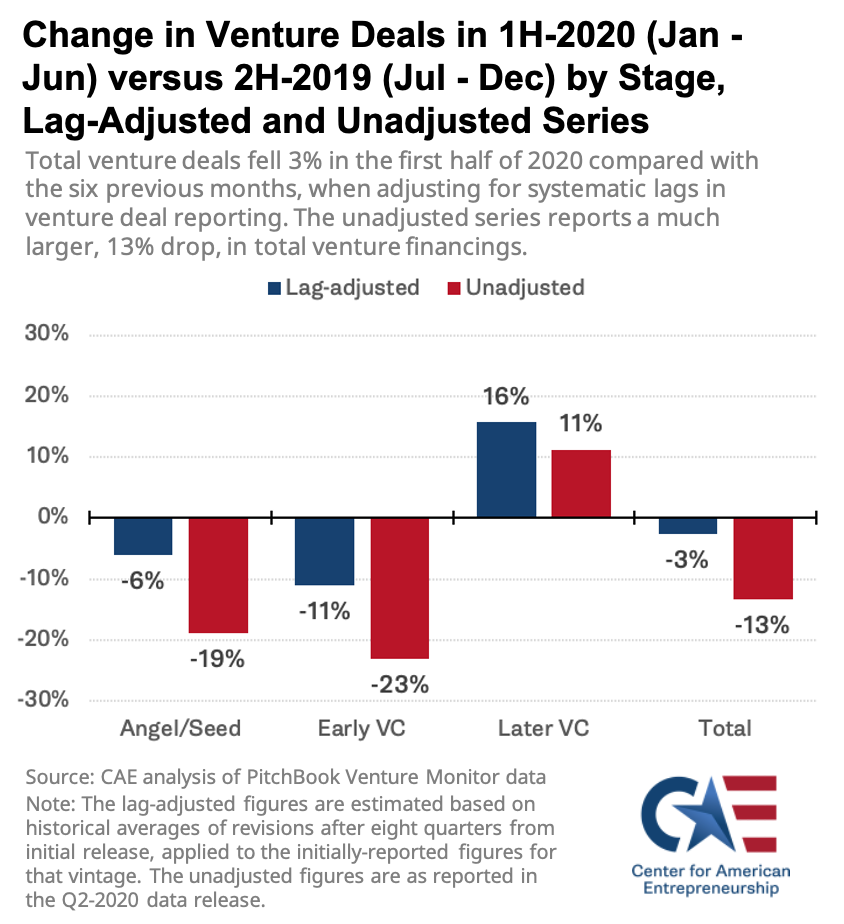

Changes in deal activity vary widely across the round stages (venture deals are “staged” as a company progresses). Deals at the very early-stage (Angel/Seed) fell 6% in the first half of the year compared with the previous six months. At the same time, deals at the Early VC stage (Series A and B) fell 11% and Later VC rounds (Series C and up) increased 16%. The change in deal stage mix may suggest that venture capitalists are putting more capital into existing portfolio companies over new investment opportunities, but further analysis is required to make that statement definitively.

No evidence exists thus far of deal discrimination for startups outside of Silicon Valley. It’s too early to say definitively since lag-adjustments can’t be applied for that analysis, but early data indicate that (i) the share of deals going to startups outside the major cities hasn’t changed during the crisis, and (ii) venture capitalists located in the San Francisco Bay Area (where half of VC resides) haven’t slowed their increasing willingness to invest in non-local companies. Venture capitalists and the startups they fund, it appears, have adjusted to working in a virtual environment like the rest of us.

This analysis provides timely and useful information to guide policymakers in navigating the current crisis. Although venture-backed firms comprise a small percentage of businesses overall (about 0.5%-1% of companies raise venture capital), they play a disproportionately large role in driving economic activity via innovation, wealth creation, and job growth. As the nation combats a severe and abrupt economic downturn, understanding the sources of growth, and how to best support them, will be critical for policymakers. The small but mighty venture economy is one of these.

Early-on, a number of pundits, analysts, and investors suggested that a severe decline in venture funding activity was possible. Consider these early narratives:

Compare these early narratives to those that have surfaced in the last few weeks. For starters, in his closely-monitored Pro Rata newsletter last month, Dan Primack, a journalist for Axios who covers venture capital and private equity, wrote the following:

Venture capital activity has persisted in the COVID-19 era, as investors and founders have accepted virtual meetings as viable alternatives to the in-person standard.

What comes next: If society returns to “normal” at some point next year, will that also apply to pitch meetings, board meetings, etc?

Why it matters: One positive byproduct of the pandemic has been that investors have been more willing to entertain deals outside their ZIP codes.

Similarly, in just the last few weeks, the following has been written:

These later narratives stand in contrast to the earlier ones. Collectively they can be summarized as stating that conditions for venture deal activity have deteriorated since the onset of the crisis, however, this decline in activity has been minor so far—especially when considered alongside the collapse occurring in other segments of the economy. My analysis is supportive of this view. Venture capitalists and the startups they fund, it seems, have adapted to dealmaking in a virtual environment.

There are two competing forces at play in the demand for information about venture deal activity: that it is timely and that it is accurate. Both have been accentuated in the COVID-19 pandemic as market participants and policymakers look to make informed decisions. In the midst of a crisis, analysts must provide decision-makers with a clear picture of what’s happening. But the simple truth is that real-time venture capital data aggregates are not accurate unless some simple adjustments are made. A non-trivial portion of deals are reported with a delay. This occurs consistently over time.

To demonstrate the systematic lag in venture deal activity, I analyze data published from PitchBook’s quarterly Venture Monitor. These reports are tabulated as snapshots of deal activity through the last day of the most recent quarter and are typically published within two weeks of that date. As subsequent quarters’ reports are issued, aggregations from earlier quarters are revised (upward). These revisions are largest in the first revision (e.g., the revision for Q1 2020 will be largest in the Q2 2020 report) and tail off from there.

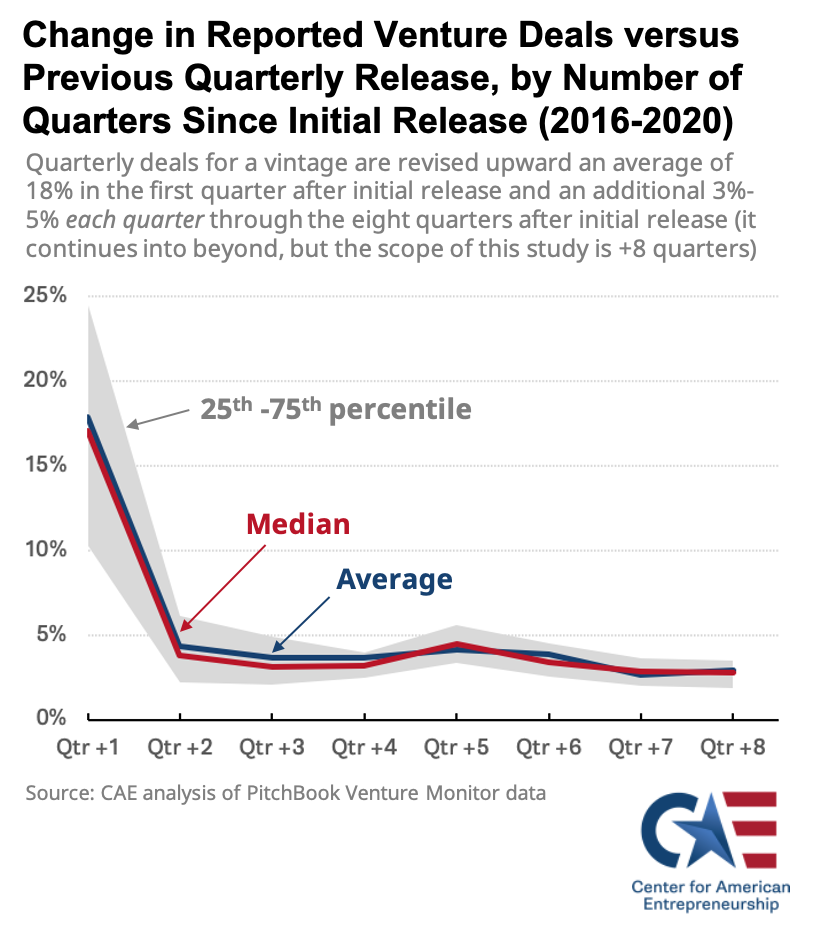

The chart below shows the percent increase in venture deal counts for a typical quarter compared with the number reported for the same vintage in the immediately preceding quarterly release. Included are values for the first through eighth quarterly revisions from the initial release, along with the average, median, and 25th-75th range of values across the reports from 2016 to 2020. Initially-reported quarterly venture deal counts are revised upward by an average of 18% in the next quarter’s publication (first revision). Revisions then continue at a pace of around 3%-5% each additional quarter into the future.

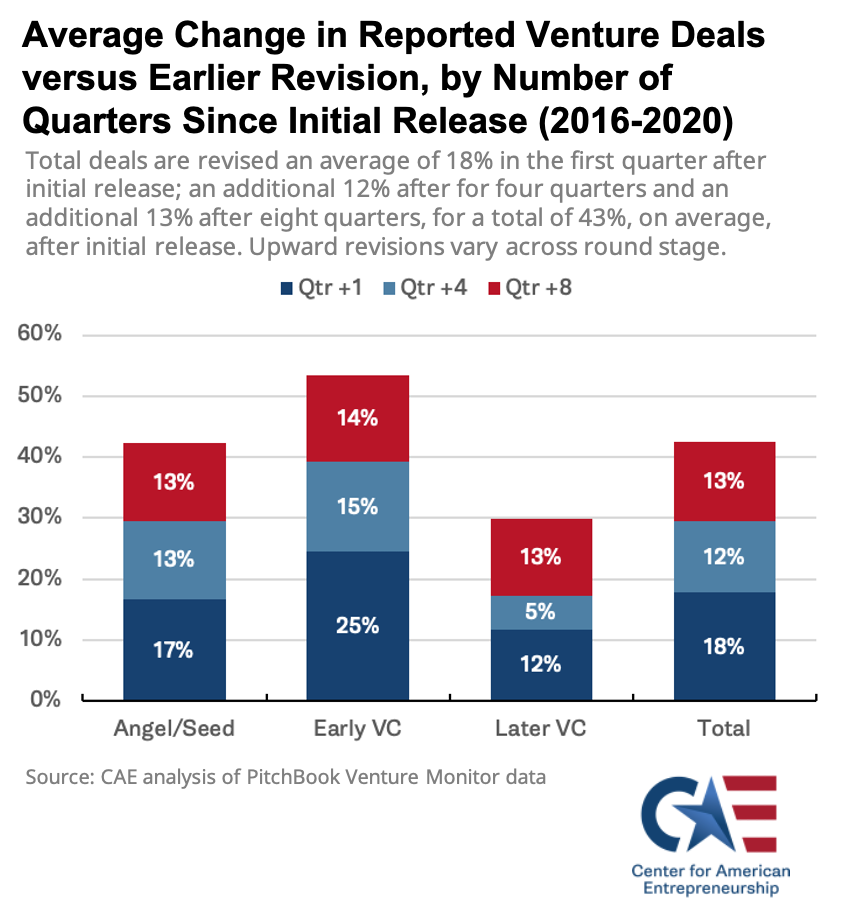

Looking at the cumulative effects of this, the data below show the average revision for total venture deals, along with the three venture round “stage” groupings (Angel/Seed, Early VC, Later VC), one quarter after first publication (dark blue), four quarters after (light blue), and eight quarters after (red). The values for each color represent the additional change compared with the preceding revision listed (color) below it. The stacked bars represent the cumulative revision after eight quarters from the initial release.

These data show that total venture deals increase an average of 18% from the initially reported levels just one quarter afterward; an additional 12% after four quarters and another 13% after eight quarters. Combined, total venture deals increase an average of about 43% from the initially reported deal counts after two years of first reporting.

Looking across the venture rounds, Early VC tends to have the largest revisions, Later VC deals the least, with the Angel/Seed rounds in the middle. Eight quarters after the initial reporting, venture deal counts for these three stages increased by an average of 42% (Angel/Seed), 53% (Early VC), and 30% (Later VC).

Since data revisions are largest in the first quarter after initial publication, recent analyses of real-time changes—for example, that compare deals in March versus December, or the second quarter versus the first—did so precisely at the time when the gap between lag-adjusted and unadjusted data is the greatest. This presents a problem with the accuracy of those analyses by overstating the magnitude of change.

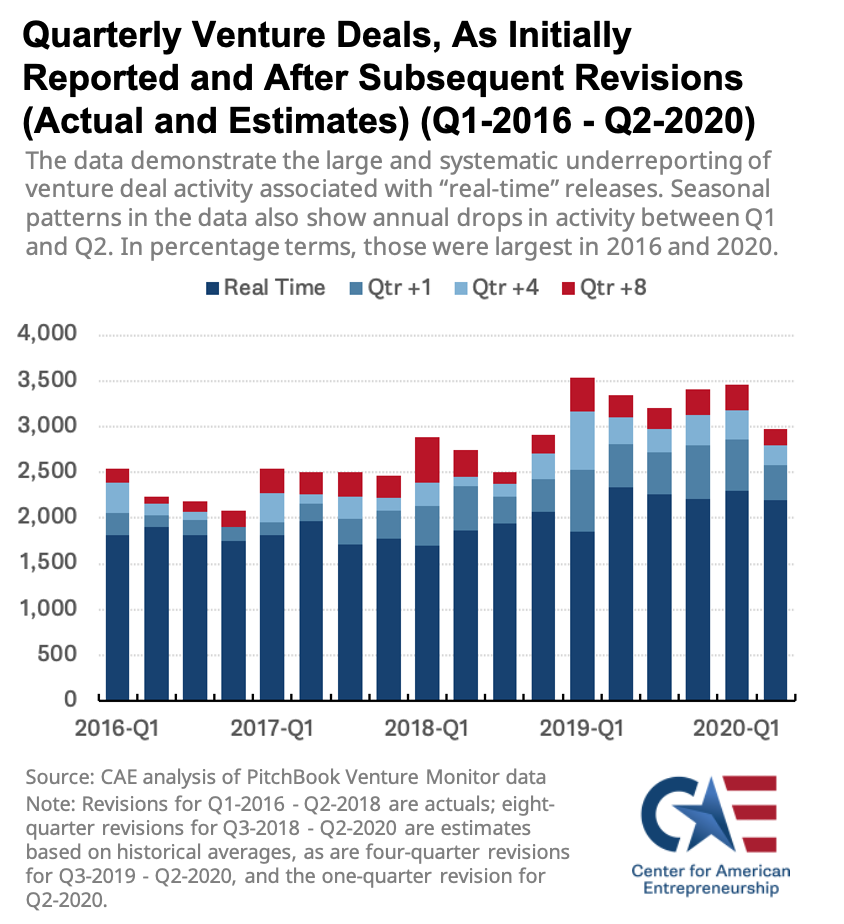

With that context of systematic reporting lags in mind, let’s now look at deal counts over time. This chart shows the total number of venture deals in the U.S. by quarter between Q1-2016 and Q2-2020, the latest release. The darkest blue bars demonstrate the counts as reported at the initial release. The lighter blue (two shades) and red bars illustrate the additional deals reported in subsequent releases (after one, four, or eight quarters). The bars are stacked to demonstrate the fully revised count at the end of eight quarters from the initial release. In instances where the revisions aren’t known because they are too recent, historical averages have been applied to estimate what those may ultimately become in the future. In this regard, all figures are on an apples-to-apples, “initial release plus eight quarters,” basis (actual or forecasted).

A few insights are revealed. To begin, real-time releases are misleading, as substantial revisions occur during the first two years after the data are first published. Second, the revisions are largest in the quarter immediately after the initial release. This makes real-time assessments of quarter-to-quarter changes in deal activity problematic because the current quarter is being reported at its lowest at the same time that the previous quarter undergoes its largest revision. Third, we do see seasonality in the data as the first quarter tends to be strongest—total venture deal activity declined between Q1 and Q2 each year in the series (about 6% on average).

Zooming in a bit, below are comparisons of changes in deal activity during the last year across the round stages: Angel/Seed, Early VC, Later VC, and Total. Comparisons will be made between the first half of 2020 (1H-2020) and the first and second halves of 2019 (1H-2019 and 2H-2019) for “previous period” and “one year ago” lookbacks. There are several reasons to avoid Q1-to-Q2 comparisons now, and instead, view the pandemic through the lens of the entire half-year. For starters, leaders in Silicon Valley had grown concerned about a potential pandemic as early as January, an issue which was on full public display by mid-February. President Trump’s primetime speech to the nation was on March 11. When the pandemic began affecting deal-making doesn’t correspond to clean Q1/Q2 demarcations. Second, an examination of seasonality in deal activity reveals that deals increased in Q1-2020 above what would be expected given recent trends. This may simply be quarterly noise in the data, but it’s also possible, perhaps even probable, that some deals were pulled forward in the first quarter as the global nature of the pandemic unfolded and investors (and entrepreneurs) grew concerned. Third, first revisions have grown larger in recent quarters compared with the longer-term average, which I apply to estimate deal “uplift” in cases where revisions haven’t occurred yet. As a result, a single-quarter comparison between Q1/Q2 in 2020 is likely to overstate a drop. Such a comparison will be more credible after the next data release (and first revision for Q2-2020), which is due out in mid-October. For those reasons, I believe Q1-2020 and Q2-2020 should be studied as a single, half-year event at this point in time.

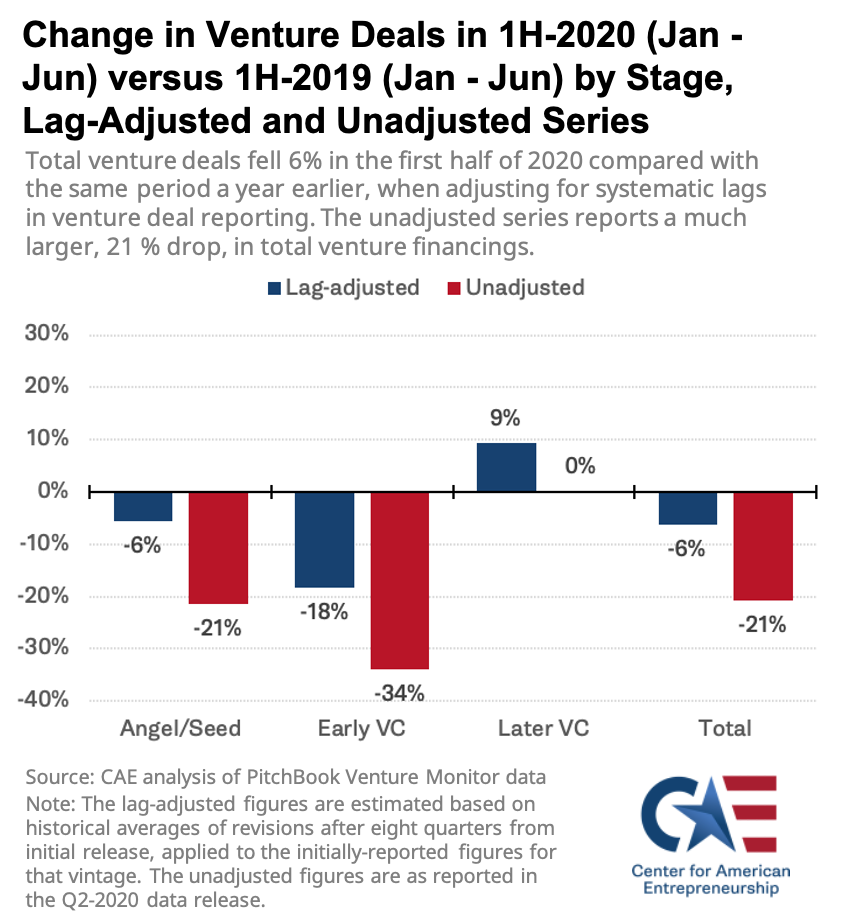

With that in mind, below are two comparisons of deal activity by stage in 1H-2020 versus both 2H-2019 and 1H-2019. The lag-adjusted series (which predicts revisions after eight quarters) is presented next to the unadjusted series to demonstrate the magnitude of error associated with many “real-time” predictions about venture deal activity.

There are a few key takeaways from the data. First, accounting for systematic lags in the data, the decline in venture deal activity in the first half of 2020 has likely been relatively small—dipping just 3% compared with the previous half-year and dropping 6% versus a year ago. Second, the declines have been uneven across the round stages. The Early VC stage has seen the largest drops while the Later VC stage has seen a sizable increase in deal activity. Although it’s not presented here, the decline in Early VC deals is a part of an ongoing trend since Q1-2019, where four of five quarters have registered declines in deal activity. Venture deal activity for the earliest stage, Angel/Seed, has declined more or less in-line with activity overall. Third, by not adjusting the data for lags in reporting, analysts and pundits have been overstating drops in real-time activity of a non-trivial magnitude. These over-estimates are large enough to challenge or even overturn conclusions some have made about the overall health of the sector. At a minimum, it demonstrates the need for a more careful analysis of venture data in real-time.

Shifting gears to the geography of venture deal activity during the pandemic, I’ll conduct two analyses using monthly deal data from the PitchBook database going back to 2012 (this database is updated dynamically; unlike the previous analysis, which used vintages of quarterly reports that are static and updated with future quarterly releases). Since the month-to-month data are higher frequency, and therefore noisy, I’ll include a statistically “smoothed” series. This allows readers to better see trends in the data.

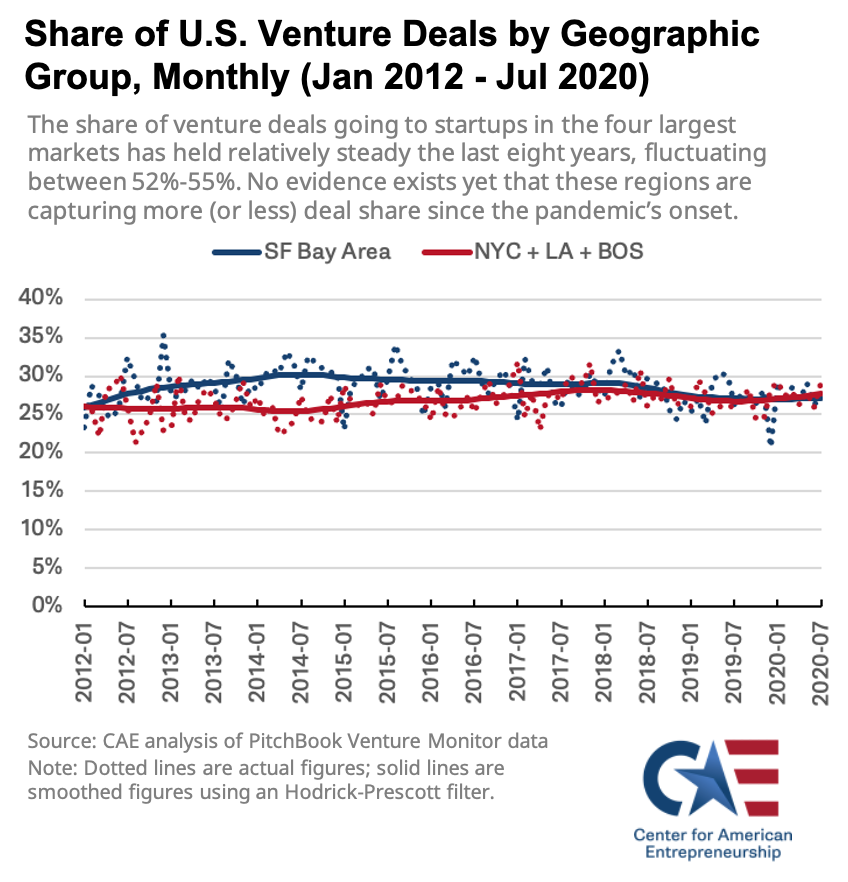

The chart below shows the share of total U.S. venture deals that went to companies in one of two leading geographic groups—(i) the San Francisco Bay Area, and (ii) the New York City, Los Angeles, and Boston metropolitan regions as a group. Combined, these four regions account for more than half of all venture deals in the United States.

The monthly data generally show a convergence between the two series over time—the share of deals going to Bay Area companies fell slightly from around 30% in 2013-2014 to about 27% today, while the share going to the second leading group of cities increased from about 25% in 2014 to about 28% today. Zooming in to 2020, the monthly data show no meaningful evidence of changes to the deal share for these regions. While it’s true the share going to New York, Los Angeles, and Boston has ticked up slightly, this appears to be part of a trend going back to around July 2019.

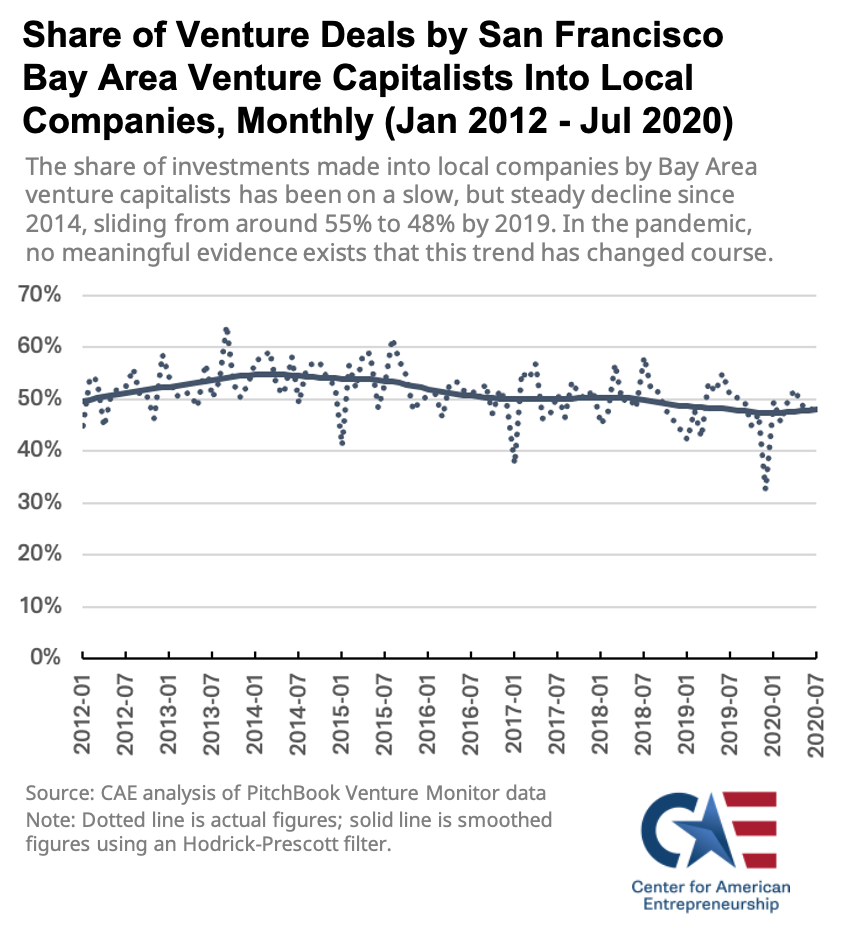

Another way to assess geographic disparities on venture deal activity due to COVID-19 is to examine the extent to which investors are making deals into non-local companies. Due to limitations in data, I’ll just look at the extent to which San Francisco Bay Area venture capitalists have been investing in companies located outside the Bay Area. It also turns out to be a reasonably good proxy for venture capital deal activity broadly since more than half of venture capital funds able to be deployed (called “dry powder”) reside within Bay Area venture capital funds.

Since 2013, Bay Area venture capitalists have been steadily more willing to invest in companies located outside the Bay Area, as demonstrated by the declining local deal share in the chart below. The percentage point changes are small—from around 55% in 2013-2014 to around 48% today—but they are nonetheless noticeable. Since the COVID pandemic took shape, the local share of deals made by Bay Area venture capitalists appears to have held steady so far.

Readers should interpret this early data with a fair degree of caution due to an inability to make lag-adjustments with the high-frequency geographic series (its accuracy relies on consistent reporting lags and biases across geography), but so far, there don’t appear to be any geographic disparities in venture funding emerging from the COVID-19 crisis. Early data indicate that the share of venture deals going to companies outside the four largest regions, which account for more than half of all deals, has held steady. Bay Area venture capitalists, which represent more than half the industry in terms of deployable capital, so far haven’t deviated from the increasing trend of funding non-local companies.

The COVID-19 pandemic has been a major disturbance to the American economy and society. It is completely unprecedented for such an abrupt and widespread shutdown to occur nationwide. Between Q4-2019 and Q2-2020, economic output (real GDP) fell 11% and payroll employment declined 9%. Broad-based unemployment (U-6) sits at 16.5% and more initial unemployment claims were filed in three months in 2020 than during the entire Great Recession. The nation is hurting. As we continue to battle the pandemic and the economic fallout, ensuring that decision-makers have access to timely and accurate information is crucial.

Though the venture capital industry, and the startups it supports, are relatively small in size and number, the impact they have on the economy is substantial. Because of this, the health and vibrancy of the sector is of high national importance. While this is always the case, it’s arguable that it’s even more important now as policymakers identify and prioritize the key sources of growth during a major economic downturn. Looking ahead, entrepreneurs are well-positioned to respond to change, particularly radical change, and therefore, will be a key factor in how the nation emerges economically during and after the crisis.

My analysis demonstrates that much of the narrative around the health of the venture economy has been overly pessimistic. Predictions of a venture capital industry in freefall have not come to pass; a collapse hasn’t occurred. In fact, overall, the sector has more or less continued its pace from the previous year. Some of these overly-pessimistic forecasts stemmed from a misapplication of data sources that are subjected to large, upward revisions shortly after their initial release. Since these revisions are systematic, they can be accounted for in a way that improves the accuracy of timely predictions, providing market participants and policymakers with the credible information they need to make decisions in a rapidly evolving environment.

Overall, the data show that the decline in venture deal activity in the first half of 2020 has been modest so far—down an estimated 3% versus six months earlier and down 6% compared with one year ago, once one accounts for the systematic reporting lags in venture capital databases. The downturn hasn’t been spread evenly across the round stages—Early VC has been hardest hit, continuing an 18-month downward trend, followed by Angel/Seed stage. Later VC deals actually expanded noticeably during the first half of the year. Early evidence suggests that startups outside of the main startup hubs (San Francisco Bay Area, New York, Boston, and Los Angeles) haven’t seen their share of U.S. deal activity decline so far during the crisis. Similarly, Bay Area venture capitalists, who control more than half of deployable capital, don’t appear to have slowed their increasing willingness to fund non-local companies.

This analysis should be interpreted with some caution. Although reporting lags in the data are persistent, variation from quarter-to-quarter can be significant—especially early on (the first revision has the widest variation). In an effort to put all quarters on an “initial release plus eight quarter revision” basis, this means that estimated figures for some quarters will be inflated while others are the opposite. Furthermore, recent trend and seasonality patterns indicate that the adjusted series in Q2-2020 may be more severely undercounted than a simple historical average adjustment would capture. As a result, the next quarterly release (the first revision for Q2-2020), due out in October, will be critical for getting a clearer read on venture deal activity in 2020.

Overall, however, the main message remains the same: venture deal activity has seen a modest drop so far in the first half of 2020 compared with the first and second halves of last year, once one adequately accounts for reporting lags in the data. Early warnings of a collapse of the venture economy were far too pessimistic. Underlying variation among the round stages, as well as some “too early to draw conclusions from” data points from Q2, present some concerns, however, future data releases will more fully clue us into what’s happening.